http://researchreport.bocomgroup.com/Strategy-210607e.pdf

----------------------------------------

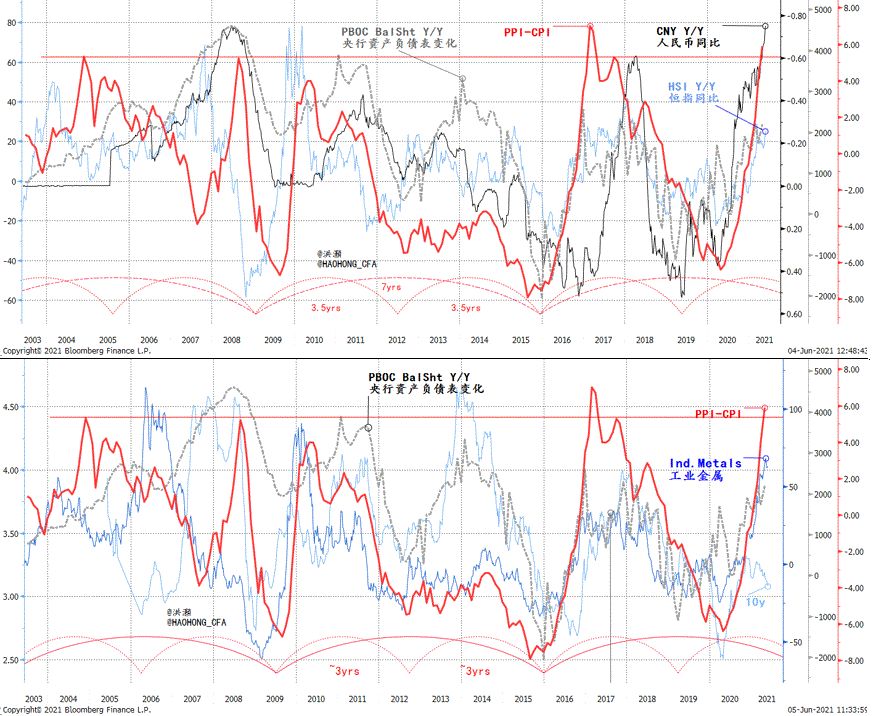

China’s PPI-CPI gap is approaching its historical peak last seen during the 2016 supply-side reform. It is another sign that the cyclical strength is about to crest. Concurrently, the PBoC’s balance sheet expansion will likely moderate. The momentum in yield, stock price and the yuan will wane. It will be difficult to offset exogenic inflationary pressure with endogenic policies. After all, China does not have enough mineral resources to sate her demands.

Nobody knows for sure how much further commodity prices will rise in the near term, as the US continues to strengthen. After all, topping is a process. But whether bond yield will rise further or not because of persisting inflationary pressure is irrelevant: if so, it will hurt the economy and stocks; if not, it will suggest a risk-off event amid a growth slowdown. Either way, it is not as conducive to take risk as last June and last November when we published our outlook reports.

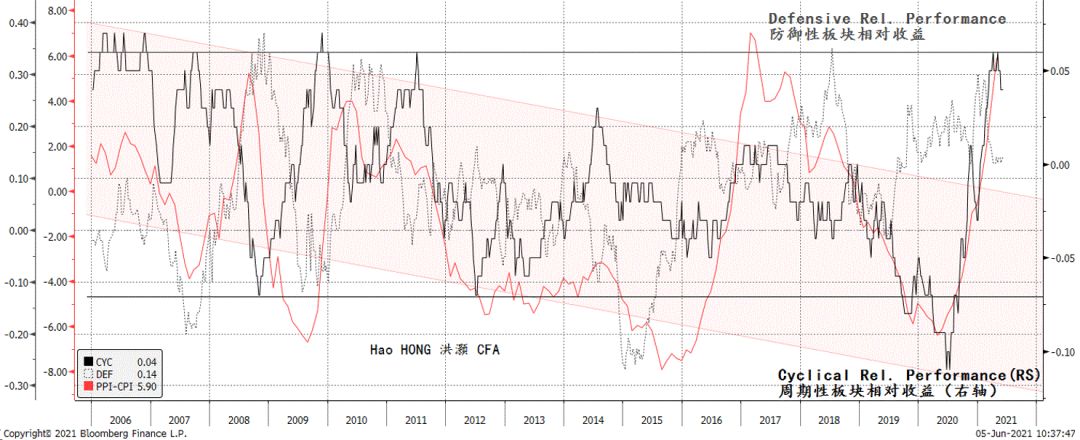

The outperformance of cyclical sectors is also peaking in tandem. The easiest money has been made. But value is yet to completely reverse its underperformance, both in cyclical and non-cyclical sectors. And the outperformance of China’s growth stocks is still elevated relative to value, and relative to China’s credit cycle. Note that cyclical does not equal value, as cyclical is defined by earnings sensitivity to economic cycles, while value is here narrowly defined by valuation multiples. It is just that when we made the value call last June, cyclicals were trading on depressed valuation and largely coincided with the value stocks in the market.

If value is still striking back while cyclical strength is about to ebb, then non-cyclical value sectors such as energy, healthcare, and utilities should offer opportunities. Meanwhile, fund managers are still huddling in defensive growth stocks such as Moutai and the entire consumer and tech sectors. Consequently, positions in commodities, energy and utilities are still nearing multi-year lows. A position rebalancing alone is enough to sustain the performance in these sectors that have done well. And the allocation to these sectors hints at a defensive posture.

The PBoC’s forex fund position has been steady since the introduction of the counter-cyclical factor in setting the yuan reference rate. Portfolio inflow has been strong due to market access reform and the prospects of China. But the PBoC’s recent warning on “one-sided” bet on the yuan appreciation suggests the incursion of speculative inflows. Such inflow can oblige the PBoC to expand its balance sheet to steady the yuan when inflation pressure is already high – a disruptive process that will be conducive to an asset bubble with costly consequences learned from June 2015. In China, stocks and bonds offer value in any global portfolio. Globally, value’s relative performance vs. growth, and commodities are still near historical lows. The return of value and the secular rise of commodities have just begun.

Figure 1: China’s PPI - CPI vs. PBoC’s balance sheet, 10Y, CNY and HSI; everything is a bet on PBoC

Source:Bloomberg,BOCOMInt'l

Figure 2: Cyclical sector relative performance is inflecting from its peak, together with PPI-CPI

Source:Bloomberg,BOCOMInt'l

http://researchreport.bocomgroup.com/Strategy-210607e.pdf

洪灝,CFA

交銀國際

2021.6.8

牛市来了?如何快速上车,金牌投顾服务免费送>>